Travel insurance and COVID-19: What you need to know

Published on: August 4, 2021

It’s impossible to predict when we’ll be able to safely travel again. Several restrictions remain in place around the world. We would like to remind you to be cautious and check the measures in force for your destination on the Government of Canada website when planning your trip. But if you need to travel outside your province of residence for essential reasons—like work, or if you have family obligations—travel insurance is more important than ever before.

Why buy travel insurance

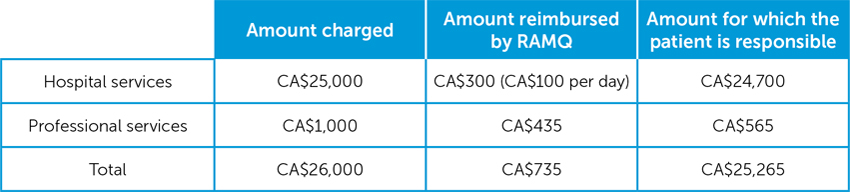

It’s a known fact that medical care is expensive. As we can see in the example below, the amounts billed following a hospital stay of just a few days can quickly add up to several thousand dollars.

And unfortunately, the patient will remain responsible for most of these costs if they don't have travel insurance, as provincial health insurance plans reimburse only a small portion of medical care abroad.

More specifically, following a sudden illness resulting from an accident outside Canada, the RAMQ will reimburse only the following costs:

- Up to CAN$100 per day of hospitalization

- Up to CAN$50 per day for care received at a hospital outpatient clinic

- Up CAN$220 for hemodialysis treatment and related medications whether the person is hospitalized or not.

Example: 3-Day Florida intensive care hospitalization following a heart attack

Source: Régie de l'assurance maladie du Québec

Insurance for medical care

More and more insurance companies are covering COVID-19, whether through individual insurance products or their regular products.

If you already have a travel insurance contract, your insurance company may have added an endorsement to it to clarify the conditions specific to COVID-19. To find out if COVID-19 is covered by your contract, read your insurance policy carefully, including any endorsements or contact the insurance company.

To learn more about Québec Blue Cross travel insurance related to COVID-19, please refer to our FAQ.

COVID-19 insurance by travel providers

An increasing number of companies have started to offer coverage insuring COVID-19 (e.g., some airlines or travel agencies). However, these policies often have limitations, particularly regarding:

- Amounts reimbursed (e.g., limit of $100,000)

- The duration of the trip (e.g., limit of 21 days)

- Destinations (e.g., insurance covering certain countries only)

Also, some insurance only reimburse expenses incurred because of a COVID-19 infection. If so, you will not be covered for any other types of medical emergencies. When booking your flight or trip, be sure to read the terms and conditions of the insurance offered to you by your travel provider, if applicable.

Checklist: What to look for when reading your policy

When reading your policy, pay attention to the following:

- Does your insurance cover medical care related to COVID-19? What are the restrictions or limitations in this regard?

- Is your destination excluded from your coverage? Does your insurance cover destinations with a level 3 (avoid all non-essential travel) or level 4 (avoid all travel) advisory from the Canadian government

- What is the maximum length of your stay?

- Are emergency medical repatriations covered?

- Do you have the option to extend your contract in an emergency?

- What is the maximum amount covered by your insurance?

Does Trip Cancellation or Trip Interruption insurance cover COVID-19?

Not all travel insurance companies have the same coverage requirements regarding Cancellation or Interruption insurance and often provide necessary product updates. We recommend that you read your travel insurance policy and review the coverage details.

Trip Cancellation or Interruption coverage offered by your Blue Cross travel insurance covers the non-refundable costs associated with the cancellation or interruption of a trip. The Optional Protection: Pandemic* insures these same costs in the event of a pandemic.

*To learn more about the Optional Protection: Pandemic, please consult the "Trip Cancellation or Interruption" section of the travel insurance policy.

Coverage extensions

The health crisis caused by COVID-19 is very unpredictable. From one day to the next, new measures could be put in place to limit the spread of the virus and protect the population. If you need to extend your stay for a reason beyond your control—for example, a border closure—you should immediately contact your insurance company to adjust the dates on your contract.

If you fail to extend it, your contract could become null and void, as most travel insurance contracts require you to cover the entire duration of a stay abroad. And if your contract is no longer in effect, your claims will unfortunately no longer be eligible, even if the costs were incurred during the initial period of coverage.

Be careful: not all contracts can be extended. Contact your insurance company to find out if you can purchase an extension from another company and obtain their authorization if necessary.

Pre-existing conditions: What it is and how to understand them

A pre-existing condition is a health problem that was present before you purchased your travel insurance or left on your trip. An injury, virus or chronic illness are just a few examples. Several pre-existing conditions aren't covered by a travel insurance contract.

In some cases, COVID-19 could be a pre-existing condition. For example, in the case of Québec Blue Cross Emergency Medical Care travel insurance, you will not be covered if you had symptoms of this illness before your departure.

Don’t forget to thoroughly read your policy before going on a trip. Knowing the terms of your contract will help you better determine whether it is safe to travel outside of your province of residence.